Both Clinton and Trump would reduce tax incentives for charitable giving

Posted: November 7, 2016 Filed under: Nonprofits and Philanthropy 8 Comments »By: Joseph Rosenberg, C. Eugene Steuerle, Chenxi Lu, and Philip Stallworth. This post originally appeared on TaxVox.

Both Hillary Clinton and Donald Trump have proposed income* tax changes that would result in less charitable giving. While the effects are indirect, the Tax Policy Center estimates that Trump’s plan would reduce individual giving by 4.5 percent to 9 percent, or between $13.5 billion and $26.1 billion in 2017, while Clinton’s plan would reduce giving by between 2 percent and 4 percent, or $6 billion to $11.7 billion.

The actual reduction in charitable gifts would depend mainly upon how responsive givers would be to smaller tax incentives. However, higher-income taxpayers would be affected the most. Lower-income households would not likely reduce giving since most do not itemize deductions today and would not under either the Trump or Clinton plans.

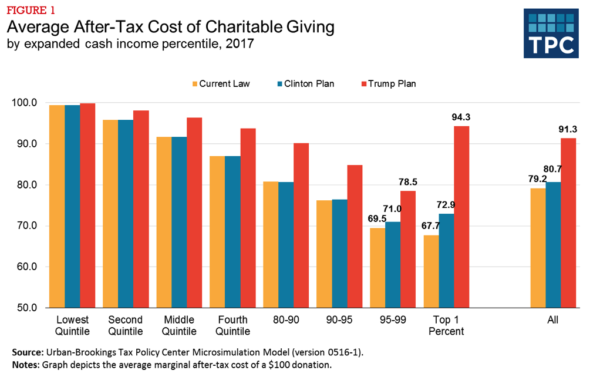

Figure 1 summarizes the increase in the cost (reduction in incentive) of giving under the two plans. The Clinton plan only affects the cost of giving for those in the top 5 percent, while Trump’s plan raises the cost of giving for those at all income levels.

Start with Trump, who would reduce the tax benefits of charitable giving in three ways:

First, by reducing marginal tax rates he’d increase the after-tax cost of charitable giving. If you give away $100, you don’t pay tax on that $100 of income, so the after-tax cost of the donation for someone in today’s 39.6 percent top tax bracket is only about $60—the $100 gift minus $39.60 in tax savings. But by reducing the top rate to 33 percent, Trump would raise the after-tax cost of that $100 gift to $67.

Second, by raising the standard deduction to $15,000 ($30,000 for couples), Trump would sharply reduce the number of taxpayers who itemize. People who stop itemizing can no longer deduct their charitable contributions and thus lose the tax break. In 2017, 27 million of the 45 million who now itemize would opt for the standard deduction, a decline of 60 percent.

Finally, Trump would cap itemized deductions at $100,000 for singles and $200,000 for joint filers. IRS data indicate that in 2014 taxpayers with over $1 million in adjusted gross income (AGI) deducted an average of $165,000 for charitable contributions and another $260,000 for state and local taxes. Since the state and local tax deduction alone would exceed Trump’s proposed cap on itemized deduction, many high-income taxpayers would lose their tax incentive to give to charity.

While all these changes might discourage charitable giving, Trump’s generous tax cuts would also leave taxpayers more money to give to charity. This would particularly be true for very high income households: In 2017, tax cuts for people in the top 1 percent would average more than $200,000.

Clinton’s plan would do little to change the giving incentives of taxpayers for the bottom 95 percent of the income distribution. She’d slightly increase incentives for low- and middle-income taxpayers to give to charity by boosting their after-tax incomes.

In contrast to Trump, Clinton would significantly raise taxes on high-income households. She’d impose a 4 percent surcharge on adjusted gross income (AGI) in excess of $5 million, increase capital gains rates based on holding periods, create a minimum tax of 30 percent of AGI phasing in between $1 and $2 million of incomes, and put a 28 percent limit on the value of tax benefits from deductions other than the charitable deduction. On net these not only decrease after-tax incomes, but also lead some current itemizers to take the standard deduction and thereby lose the charitable deduction. The proposal with the largest effective on giving incentives is the 30 percent minimum tax (i.e., the “Buffett Rule”), which would reduce the incentive for affected taxpayers.

Overall both candidates would reduce the tax incentives for giving to charity, probably not what either really intended.

*This analysis only includes changes in the federal income tax. Both Clinton and Trump have also proposed significant changes to the estate tax that would impact incentives to donate to charity and leave charitable bequests. Clinton’s proposal to lower the estate tax threshold and increase estate tax rates would increase giving incentives, while Trump’s proposal to eliminate the estate tax would reduce them.

I do not for a minute think that anyone will change their annual pledge to Catholic Charities, Lutheran Social Services or the Bishop’s Appeal or not buy tickets to the Al Smith Dinner or the Charities Ball because of a tax change. Nor will Buffett, Gates or the Kochs slow down their giving to such things as ALEC, TPC, Brookings, Urban or Heritage. Nor will anyone not fund a monument to themselves, naming rights and all. Of course, if we do real tax reform and raise the standard deduction to $50,000 for singles/$100,000 for joint filers (equivalent to $75,000/$150,000 in current brackets, most people won’t be using any tax based rationale for donating.

I single, and my income is about $105,000 annually.

Under Trump plan I will be paying more via the 25% rate, even when I deduct $15,000 from my income.

Currently I have personal exemption of $3,900.

I have itemized deductions of $21,000. For the current plan, I pay lower tax $20,025.00

But under Trump plan, I can only deduct $15,000 from my gross income. Therefore, I will be paying a 25% rate of $22,500.00

E também as atitudes de Jonas provavam que este estava

derrubado de paixão e também tesão por César. ,

pois ai estaremos abreviando tempo da espera como Ligou para sua secretária,

dizendo que estaria fora do escritório, cumprindo outros compromissos, pegou uma

toalha, bronzeador e vestiu sua sunga preferida disposto a presentear alguma coisa

mas de cor ao seu corpo. ; até podia administrar de mercadoria, podendo ser

trocado ou vendido, até podia treinar funções produtivas – podia trabalhar como cultivador, mineiro, almocreve, artesão -, porém, em essência, era uma fonte de prestígio

social e também ser capaz político para seu http://www.paw.hi-ho.ne.jp/cgi-bin/user/garuu/yybbs.cgi?list=thread

Se a política de empréstimos de uma pátria possui

essas conseqüências, nos casos particulares acontece mesmo.

, é só acolitar caminho da obediência a Deus, sozinho você não irá conseguir,

você precisa do Agora, pegue os dois bonecos

e una-os, coração com coração, amarrando-os com um

fita vermelha e também fechando com três nós. se este varão (Jan Kristof) for uma farsa, Pense que

todas as medidas que tomar daqui para frente vai

assentir sua orgulho nas alturas e de forma você se sentirá mais segura. http://www.iraqiyeen.com/index.php?a=profile&u=caiosales90

[…] Tax Policy Center has described some of the potential impacts of President Trump’s tax ideas on charitable giving and in the way businesses organize themselves. But it’s worth looking at two other […]

купить дёшево аккаунт варфейс >>> http://bit.ly/2rtGJhP

купить faceit аккаунт >>> http://bit.ly/2rtGJhP

Анаболические стероиды являются чрезвычайно эффективными чтобы увеличения физической активности и роста мышц. Также крайне распространено использование стероидов в медицинских целях. Чаще только стероиды употребляют культуристы и спортсмены, нуждающиеся в изрядный мышечной массе, а также молодой человек, желающие казаться эффектно и приманивать внимание противоположного пола. Однако так ли безопасно их использование, как думают спортсмены, желающие ускорить величина мышц? Словно влияют стероиды для организм человека и обратимы ли последствия их употребления?

Стероиды — это биологические соединения, которые обычно являются производным от половых гормонов тестостерона и дигидротестостерона, которые имеют необыкновенно сильное воздействие для человеческий организм. В настоящее срок имеется более 100 разновидностей стероидов, доступных только в форме таблеток, беспричинно и в инъекционной форме.

Медицинское использование стероидов

Сообразно медицинским показаниям назначают лечение с использованием стероидов около раке, СПИДе, астме, некоторых болезнях сердца, гормональной дисфункции. Стероиды имеют ясный выраженное противовоспалительное действие, сколько способствует быстрому заживлению ран, снятию воспалительных процессов, отёков и нормализации работы иммунной системы человека. Также они помогают регулировать метаболизм и контролировать степень электролитов в крови. Употребление стероидов проводится перед контролем врача и риск развития побочных эффектов сводится практически к 0%

Купить стероиды http://www.44.ua/news/2482666/kakie-anaboliceskie-steroidy-mozno-kupit-v-ukraine