Can One Think Charitably About The Bryce Harper Deal?

Posted: July 9, 2019 Filed under: Uncategorized Comments Off on Can One Think Charitably About The Bryce Harper Deal?This column first appeared on TaxVox.

As a long-time baseball fan, I’m happy that my office moved closer to the Washington Nationals ballpark, where I expect to take in more games this year. But I’ll do so with some misgivings, in part because of how the Nationals and their former star Bryce Harper missed an opportunity. Not because Harper left DC for the rival Philadelphia Phillies, but because Harper and the teams he negotiated with whiffed on their chance to send an important message about acting charitably toward their communities.

For months, there appeared to be large dollar differences between the kind of contract Harper sought and the contracts teams were willing to offer. Eventually, Harper signed with the Phillies who paid him $330 million over 13 years. However, there was a missed opportunity to bridge the gap between the parties. For instance, the team could have proposed to donate much of the difference to charities, a foundation or a donor advised fund at a community foundation to support Harper’s charitable efforts. This would not only have benefited others, but likely returned substantial value to Harper and the team’s owners through enhanced goodwill in the community.

The same principle could apply to other sports negotiations. For instance, a team could use a similar charitable transfer to hang onto a popular older player who is less productive than he once was and whose high-dollar re-signing would create potential problems with salary caps and luxury taxes. The team could pay him less in salary and shift some of the difference to his favorite charity.

Even beyond sports, donations to charity can be a great way to mediate differences in all sorts of disputes. It can work for business contracts, lawsuits, or even divorces. Because of their visibility, however, athletes and team owners have a unique opportunity to demonstrate how to convert dollar disputes into charitable benefits.

Yet, a foundation official who previously worked for a major sports team told me that she had never seen charitable giving in the playbook of either teams or professional athletes. But just as Bill and Melinda Gates drove charitable giving among fellow billionaires through their “Giving Pledge” initiative, a group of team owners could do the same among their sports connections. They could even hire famous retired athletes who have a record of generosity to lead the effort.

Let’s face it, communities contribute substantially to these owners and players, not just by buying tickets but through considerable taxpayer support. The federal government exempts Major League Baseball from antitrust laws. State and local governments often grant teams concessions through tax breaks, zoning rules, development of roads or public transportation to ballparks, and much more. And much of the income of successful team owners comes in the form of accrued capital gains that may never be subject to income tax.

Of course, some players and team owners already are generous donors to their communities—often quietly. But the press rarely provides a thorough accounting of owners’ and players’ charitable efforts. Indeed, the pizza joint that donates $10 per home run gets vastly more attention than the charitable giving—or lack of giving—by athletes and team owners.

A charitable gift in lieu of a portion of salary can raise tax and other issues. For instance, the money may be more valuable if it is first given to the player, who would in turn donate it to charity (the IRS might deem the contribution to essentially be the player’s compensation in either event). And, this approach would also raise the issue of whether the donated money would be counted as compensation subject to league rules on salary caps and luxury taxes. Those challenges could be overcome, and the likely outcome favorable because owners would not want to be seen as creating rules that “taxed” charitable contributions.

The real issue, though, is whether some future Bryce Harper will step to the plate and hit a home run for the community. Let’s hope so.

Alice Rivlin: The George Washington of the Congressional Budget Office

Posted: June 26, 2019 Filed under: Uncategorized Comments Off on Alice Rivlin: The George Washington of the Congressional Budget OfficeOn June 21, the family and friends of Alice Rivlin joined with much of Washington’s public policy community to celebrate her life and extraordinary public service. This note represents only a small addition to the outpouring of tributes made to her.

This column first appeared on TaxVox.

Alice Rivlin, who passed away on May 14, was among the greatest public servants of the modern era. I admired her so much that I once told her I’d quit my job and join her campaign if she would run for president. Even in a likely loss, it would be a winning proposition, I asserted, to finally have someone honest and forthright in a presidential debate.

A few years ago, George Kopits, now at the Wilson Center, asked Alice and me to write chapters on the Congressional Budget Office (CBO) for a book he edited on independent fiscal institutions. Alice was as famous among budget experts abroad as she was in the US for her role as founding director of CBO–widely regarded as the best and most independent fiscal institution in the world.

Along with her immediate successors, Rudy Penner and Robert Reischauer, Alice created two crucial roles for CBO. First, of course, it assessed the macroeconomic and budgetary consequences of existing and new policies. But despite a fair amount of Congressional opposition, CBO did more than cost estimates. It also assessed the efficiency and distributional effects of programs.

Her chapter, “Politics and Independent Analysis,” (Restoring Public Debt Sustainability: the Role of Independent Fiscal Institutions, Oxford, 2013) described how an institution could tell politicians what they didn’t want to hear and still thrive. Few other countries, even the most democratic, have succeeded in creating a fiscal institution with the same degree of independence as CBO. And in today’s political environment, it is risky to take such institutions for granted.

Increasingly, these non-partisan technocratic organizations are threatened by those who want to control the policy narrative. An effort to create an independent fiscal institution in Hungary, first headed up by George Kopits, became one of the first casualties of Prime Minister Viktor Orban’s government. In the US, CBO is increasingly important as executive branch agencies become more politicized by presidents who want to control the public narrative. In her 2017 keynote speech at an OECD conference, Alice reaffirmed her lifetime devotion to principles of good governance at a time when they are being challenged by governments at home and abroad.

Alice always was being asked to take on new tasks. Fortunately, her commitment to good citizenship often overcame her reluctance. A few years ago, already in her eighties, she agreed to temporarily lead the health policy group at the Brookings Institution– not because she wanted to, but because she thought it was important.

In the late 1990s, Alice reluctantly took on the thankless role of chairing the District of Columbia’s Financial Responsibility and Management Assistance Authority (known as the Control Board). Carol Thompson Cole, now the president and CEO of Venture Philanthropy Partners (an organization that invests in children and youth throughout the Greater Washington area) helped convince Alice to take on the difficult task. Carol told her the board needed her prestige and trustworthiness to establish the stability and stature it needed to get the District’s finances under control. Once she accepted the role, Alice used her skills and good will to help set the District on a solid fiscal path.

One of my fondest Alice stories comes from Bo Cutter. In the early days of Bill Clinton’s presidency, Bo, now at the Roosevelt Institute, was a senior White House economic adviser and Alice was deputy director of the Office of Management and Budget.

Like candidates before him, Clinton had promised more in his campaign than he could deliver. In his case, he pledged more spending and tax cuts even as he pled for fiscal sanity. At an early meeting of budget advisers, Clinton was furious that by laying out the fiscal facts, his staff was forcing him to backtrack on his promises. Alice responded, “But Mr. President, you are president and now we have to decide.” As they were leaving, Alice explained to Bo that “the most relevant training [for her job] is being a mother.”

Of course, these are only a few of the many great stories about Alice, one of the most brilliant, modest, resourceful, and effective policy makers and analysts I have had the privilege of knowing.

Thanks to Carol Thompson Cole, Bo Cutter, and George Kopits for sharing these anecdotes.

The Legacy of George H.W. Bush: Some Further Notes

Posted: December 17, 2018 Filed under: Uncategorized Comments Off on The Legacy of George H.W. Bush: Some Further Notes“For where the rewards of virtue are greatest, there the noblest citizens are enlisted in the service of the state.” – Pericles’s Funeral Oration, as told by Thucydides

At least from the time of ancient Athens to this day, we extol the virtuous actions of those who have died, less as a tribute to them—after all, they have passed on—than as a challenge to ourselves and our youth to find actions to emulate. In recent decades, we have also become much more sensitized to the danger of sentimentalizing history by ignoring the limitations and prejudices of our past.

In this vein, to the many tributes made on behalf of our 41st president, I want to make two observations on the president’s legacy that have become especially relevant at a time when public officials attack good budget and tax policy, and private citizens attack those who engage in major philanthropic endeavors or public service, modern-day forms of “noblesse oblige.”

In doing so, I don’t mean to discount the continuing cost of his failures, as reflected in Lee Atwater attacks, race-baiting Willie Horton ads, and nonsensical “No new taxes” pledges. This is a time to celebrate the good a person has accomplished.

Memories of Bush’s pragmatism on budget and tax policy

President Bush’s interests and strength in working with people was nowhere better served than in the field of foreign affairs. But that skill—and willingness to do the right thing, even at personal cost—also played out in budget and tax policy.

Much attention has focused on the controversy surrounding the president’s willingness to violate his “No new taxes” pledge in agreeing to a 1990 budget agreement. Less attention has been paid to the ways that Republicans have largely repudiated that budget agreement, while Democrats have largely used that repudiation to exaggerate their own success through a slightly smaller budget agreement in 1993 under President Clinton.

Consider: each agreement reduced the deficit by $500 billion over five years, but in 1990, $500 billion was larger in real, inflation-adjusted, terms and as a share of GDP. Both bills significantly expanded the earned income tax credit, but the 1990 increase was larger, though phased in partly during the Clinton administration. Perhaps the most important part of both bills was acceptance of a so-called pay-as-you-go rule that in the 1990s essentially required new tax cuts and new entitlement spending to be paid for.

These two bills represented the primary legislative budget achievements of the decade. What then brought down the deficit so much by the turn of the century? A temporary stock market increase led to a large increase in revenues through capital gains recognition. Health cost growth slowed temporarily through the expansion of health maintenance organizations and preferred provider organizations. And the baby boomers entered peak earning and productivity years. Finally, there was a long stalemate on major give-away legislation reinforced by the pay-as-you-go rule.

George H.W. Bush’s pragmatism also had a significant effect on the successes of the Reagan administration. At the start of that administration, a war broke out between the more ideological and the more pragmatic sides of that administration. As is usual with almost all administrations, the ideologues eventually move on, as their strength comes from protesting and tearing down, not governing.

Among the pragmatists who accompanied then–vice president Bush to Washington and helped create many of the domestic successes for President Reagan was a group sometimes called the Texas Mafia (an appellation often meant to be friendly), who knew and often had worked with the vice president. These included James Baker and my friend and then-boss John E. (Buck) Chapoton.

Baker’s successes as White House chief of staff and as Treasury secretary (later secretary of state under President Bush) are well known. Less recognized, Buck played a significant role as an assistant secretary in leading the Tax Policy Office at Treasury through 1982 and 1984 deficit-reduction agreements and 1983 Social Security agreements—all of which had tax increases. He then negotiated the minefield that allowed us on the Treasury staff to develop the tax reform study of 1984 that led to the Tax Reform Act of 1986.

Buck, who at one time lived in Houston around the corner from the future president, also tells me a story about an issue that came up in the early 1980s and has been rejuvenated recently in the Trump administration: attempted Office of Management and Budget overview of Treasury regulations. Buck decided to call the vice president, who then had oversight over deregulatory matters.

Buck says he started having second thoughts about his boldness in making the call. He realized he could no longer call him “George,” and, when the vice president got on the line, Buck felt the need to stand up and address him by his title. He explained to the vice president that slowing down interpretative, rather than policy, regulations would hurt, not help, taxpayers who needed the information. The vice president had no problem accepting this pragmatic advice, and whether he later interceded, the problem for the most part was solved.

These examples show how success follows from a willingness to work and listen to people, a lack of fear of having smart people around oneself, and a readiness—no, more than that, a sense of obligation—to tackle important problems when they need to be tackled.

Extolling those who help society from a position of advantage

In many policy arenas, it is common to attack those with power and wealth. After all, often that power or wealth may not have been earned or distributed fairly by some standards, as in the case of inheritance or luck or being among the winners in a winner-take-all economy.

Those attacks often extend to what I will call the “oblige” side of “noblesse oblige”—the obligations rather than entitlements of the wealthy. Why should buildings be named after contributors or charitable deductions be allowed, or, for that matter, the famous be extolled for actions no finer than those taken daily by some of our relatives?

The answer, I think, obvious. We want those who succeed or have success handed to them to feel great obligation toward society. We want them to join, not separate, themselves from us. We want them to join the military when action is required. We want them to share their wealth.

Someone who makes $1 million and gives it away to true charitable causes contributes more to society than someone who makes the same amount and pays $300,000 in taxes. Removing incentives to give, an increasing tendency in modern tax policy, expands alternative uses of their money for conspicuous or wasteful consumption, empowering their heirs, or exercising political power to further aggrandize their wealth.

Antitrust and tax policy can and should focus on the entitlement or noblesse side of noblesse oblige, but such policies must build up wealth from the bottom, not simply level it from the top.

When the George H.W. Bushes of the world feel compelled to return to society some of the gifts it has made to them, and to be willing to accept the cost of rightful action, we’re all better off. Thank you, Mr. President, for this reminder in the midst of today’s raw political circus.

Regulation, Kavanaugh, Trump & the Indexing of Capital Gains

Posted: September 24, 2018 Filed under: Uncategorized Comments Off on Regulation, Kavanaugh, Trump & the Indexing of Capital GainsThis column first appeared on TaxVox.

The issue of government regulation promulgated by unelected officials is central to many of today’s political and policy debates. It has surfaced in the confirmation battle over Supreme Court nominee Brett Kavanaugh, a strong critic of regulatory actions that are unsupported by legislative or constitutional authority. And we see it in the Trump administration’s contradictory regulatory initiatives: aggressive deregulation when it comes to environmental law paired with enthusiastic administrative efforts to reduce taxes on capital—absent clear legislative authority.

While the nation’s regulatory wave crested four decades ago, long before President Trump, the pattern has always been inconsistent. President Jimmy Carter jumpstarted the modern deregulatory push by cutting red tape for everything from airlines to home-brewed beer. Every president since has laid claim to at least part of the antiregulatory mantle. Yet, every recent president, including Trump, has also attempted to achieve policy goals through administrative power.

The current administration has been especially enthusiastic about using regulations to achieve tax policy ends. Senior White House advisers have asserted that Treasury and IRS can issue regulations to provide for the indexing of capital gains. The president himself has asked Treasury to liberalize the treatment of required distributions from retirement plans. Both share a common goal: to cut taxes on returns to wealthholders without enacting a statute.

In truth, presidents and political parties favor regulation mainly when it when it advances their own agenda, regardless of the number of pages it adds to the Federal Register. Interestingly, both presidents Trump and Obama have turned to administrative and regulatory initiatives in frustration when they felt they could not achieve their policy goals with Congress. And, when it comes to the sausage they do seek and get from Congress, their antiregulatory fervor falls by the wayside; witness all the regulation that IRS still struggles to issue around the Tax Cut and Jobs Act of 2017.

But what are the criteria by which an affirmative decision to regulate should be made? In theory, they are twofold: benefits should exceed costs and the actions should be constitutionally and legislatively allowed.

Using regulation to interpret the law can simplify life for taxpayers by providing rules surrounding the large number of possible transactions and arrangements into which they may enter. Such a requirement is often implicitly, if not explicitly, allowed by the legislation itself. While the law may not pass the benefit-cost test, regulations to taxpayers on how to be law-abiding usually does. Though the line between interpretation and exercising authority ceded in legislation is never perfectly clean, the Treasury and IRS have always viewed their guidance as mainly interpretative.

Yet, most administrations, not just the current one, often are tempted to wade into technical tax issues about which they have limited knowledge. A strong Treasury Secretary or Assistant Secretary can constrain such efforts, sometimes by making clear that meddling is unnecessary and potentially politically dangerous.

Extending to administrative agencies non-interpretative, legislative-type authority raises more complicated benefit-cost and statutory authority questions.

The Constitution explicitly requires that the President, not the Congress, “take care that the laws be faithfully executed.” Even if it didn’t, Congress has neither the time nor the expertise to execute laws, and implementation inevitably requires discretion. Anyone who has ever sat at a congressional drafting session knows how much Congress leaves unspecified in legislative language. Long before a tax bill becomes law, congressional staff have begun consulting with Treasury and other agencies over how to fill in the inevitable gaps in the statute.

Bottom line: Think twice before generalizing about the costs or benefits of regulation or even its constitutional basis. And remember that the political and ideological arguments for or against regulation, particularly as something good or bad in and of itself, tend to be selective and supported by weak legal and economic reasoning. Mostly, though, remember that the best way to avoid bad regulation or rule making is to avoid bad law making.

Individuals Pay Very Little Individual Income Tax on Capital Income

Posted: September 13, 2018 Filed under: Uncategorized Comments Off on Individuals Pay Very Little Individual Income Tax on Capital IncomeThis column first appeared on TaxVox.

Most capital income earned never is taxed at the individual level, in part because assets are often not sold and their gains never subject to income tax, in part because capital income benefits from a long list of tax preferences, and in part because of outright evasion.

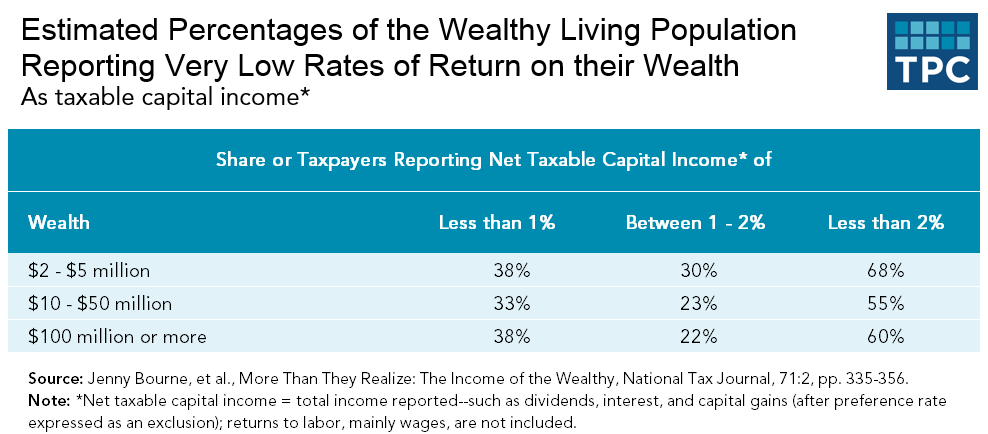

In a recently-published study, Jenny Bourne, Brian Raub, Joseph Newcomb, Ellen Steele, and I used estate tax data linked to individual income tax return data. In the study, we found that most wealthy individuals report an effective taxable return on their wealth of less than 2 percent on their individual income tax returns, with the richest filers reporting the lowest returns. That is, for each $1 million of wealth, the annual amount of taxable dividends, interest, capital gains, and other returns is less than $20,000. Among those with more than $100 million in net worth in 2007, close to 40 percent reported annual taxable returns of less than 1 percent of their wealth. More than two-thirds reported taxable returns of less than 2 percent.

These results are similar to what I found in a study covering the more inflationary 1970s. In yet another study, I found that a select group of owners of businesses and farms subject to estate tax reported even lower taxable returns. And in a book published in the early 1980s, I showed how net income from capital reported on all individual tax returns was less than one-third of total capital income in the economy.

These results are similar to what I found in a study covering the more inflationary 1970s. In yet another study, I found that a select group of owners of businesses and farms subject to estate tax reported even lower taxable returns. And in a book published in the early 1980s, I showed how net income from capital reported on all individual tax returns was less than one-third of total capital income in the economy.

Keep in mind, regardless of what they report on tax returns, top wealthholders often achieve very high actual returns on their assets. The merely wealthy commonly earn stock market returns of 7 to 10 percent per year, while truly rich investors often attained that status by earning even more. Warren Buffett revealed in one income tax return that he recognized only about 1/50th of 1 percent of his wealth as taxable income even though his primary asset, Berkshire-Hathaway stock, had been earning about 10 percent annually.

How do those with capital income achieve such low taxable earnings?

- Capital gains are not taxed until the assets are sold and the gains realized, providing an incentive to hold onto assets as they appreciate. As long as they are unsold, there is no taxable income to report.

- They take advantage of tax preferences. Real estate investors, for example, can defer taxable gains by swapping one piece of property for another through a “like-kind” exchange. The preferential tax rate on long-term capital gains acts as an effective reduction in taxable income, as it has been in most years when the preference was provided as an exclusion.

- Asset holders may avoid capital gains taxes by arbitraging tax laws. For example, they may offset gains with losses. Or they may establish tax shelters that produce current deductions in exchange for lightly taxed or untaxed capital gains.

- The returns from homeownership—the rent saving that comes from equity ownership—are not taxed.

- Retirement saving is heavily favored by the tax system, meaning that asset appreciation and capital income may not be taxed as they occur.

Homeownership and retirement saving provide the primary opportunities for middle-income and moderately-wealthy households to avoid or defer tax on capital income. As a result, they, too, pay limited tax on their returns from capital.

But for very wealthy individuals, the most common tax-avoidance strategy is simply to not sell assets at all and never realize the taxable gains. For example, a shareholder in a publicly traded company may accrue capital gains over time that remain untaxed until she sells her shares. If she holds the asset until death, those accrued but unrealized capital gains are excluded altogether from tax. The assets passed along as a bequest will have basis equal to the value at the date of former asset holder’s death.

Because so little capital income is taxed through the federal individual income tax, corporate and estate taxes have been important tools for taxing those with significant wealth. However, Congress has cut both those taxes over recent decades, most recently in the 2017 Tax Cuts and Jobs Act. Those reductions may have a far larger impact on the effective tax rate on capital income than changes in the statutory individual income tax rate since that levy only applies to income that is realized.

Unfortunately, the fight over capital income taxation usually focuses on how much is collected rather than on the most equitable or efficient way to tax it. Advocates on each side often will accept capital tax increases or decreases any way they can get them. Nor do the debates result in consistent treatment of people at different levels of wealth.

The Trump Administration reportedly is considering reducing taxes on capital income by indexing capital gains taxation for inflation. But at this point, the better question may be how best to distribute the taxes borne by capital owners, not simply how to tax some of them less.

Indexing Capital Gains For Inflation Addresses A Real Problem But Ignores Existing Law

Posted: August 23, 2018 Filed under: Uncategorized Comments Off on Indexing Capital Gains For Inflation Addresses A Real Problem But Ignores Existing LawThis column first appeared on TaxVox.

The idea of indexing capital gains for inflation is getting a lot of attention these days. Larry Kudlow, who heads the White House National Economic Council, has long suggested Treasury should do this by regulation, while several members of Congress have introduced bills to make the change by modifying the tax code. Exempting purely inflationary gains from tax can be a good idea in principle, but easily flawed in practice. To understand the consequences of such a shift, it is helpful to think about it in terms of a revenue-neutral tax change, not merely another budget-busting tax cut.

In a revenue-neutral context, indexing the basis of assets in computing capital gains could create significant winners and losers among investors. Ordinary shareholders could come out ahead, while private equity firms could be big losers. The effects would largely be dependent on rates of inflation and market returns.

First, though, some background: The argument for indexing rests on the principle that the income tax is meant to tax real, not nominal, income. If my investment returns 8 percent and inflation is 8 percent, then my real income gains are zero. Why should I pay tax on zero income?

To make matters worse, if we taxed all returns to saving with no offset for inflation, we could enormously overtax nominal returns to capital. If returns averaged 8 percent and but inflation was 4 percent, subjecting the full 8 percent nominal return to tax would essentially double the statutory tax rate on capital income.

In the 1984 Treasury study that led to the Tax Reform Act of 1986, these considerations led us to propose indexing the basis of assets that generate capital gains for inflation. But we attempted to apply the principle consistently. We would have indexed capital gains but also indexed other elements related to investment returns. We would have indexed depreciation allowances for inflation but also would have repealed the investment tax credit and set depreciation allowances to approximate economic depreciation. We also would have indexed interest receipts and interest payments for inflation.

Building on the old Treasury plan, imagine Congress indexes the taxation of capital income in a way that would neither gain nor lose revenues over time. Such a change would have many effects on the taxation of investment, but here are two significant ones:

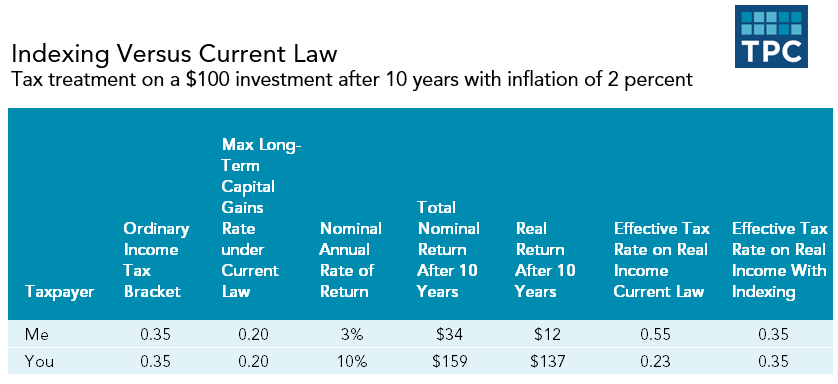

First, such a reform could redistribute the tax break to investors who tended to get lower returns over time from those who through luck or skill were big winners. Consider a reform proposal that substitutes indexing of capital assets for the preferential tax rate on long-term capital gains. The following table shows how this might work for a specific example.

For example, suppose you and I invested $100 ten years ago. Inflation was 2 percent annually over the period, and assume that we’re both in a 35 percent income tax bracket with a current maximum tax rate on long-term capital gains of 20 percent. Suppose that I earned a 3 percent nominal annual return per year and you made 10 percent. With indexing, we’d both reduce our gains by $22 (the amount of inflationary gain on the $100 investment). That would leave me with taxable income of about $12 out of my $34 profit. But you’d have taxable income of $137 out of your $159 gain (10 percent compounded over 10 years). With indexing and no preferential tax rate on capital gains income, we’d both pay the 35 percent rate but only on the real income amounts. Under current law, we’d each pay the 20 percent tax rate on our nominal capital gains ($6.80 tax for me and $31.80 tax for you). This translates in an effective tax rate on my real income of 55 percent and 23 percent for you. So, this proposal would treat all inflation adjusted returns the same, compared to current law, which favors investors with large inflation-adjusted gains.

Second, in a period of high inflation and moderate appreciation of assets, indexing gains for inflation while ending other preferential tax treatment for capital income might lower the amount of such income subject to tax. To illustrate this point, note that if inflation were 8 percent per year and the value of an asset increased at 8 percent per year, there would be no tax due under an inflation-indexing regime, but a positive tax liability under current law (even with the preferential tax rate on long-term gains). In contrast, in a period of low inflation and unusually high appreciation of asset values, such as in recent years, the indexing proposal likely would increase effective tax rates.

To see whether advocates really believe in the principle of excluding inflation from taxable gains, ask them if they would be willing to accept those consequences. In effect, would private equity and hedge fund managers be willing to transfer some of their existing tax breaks to help average investors?

I could make a solid case that such an exchange would be fairer and more efficient since it would provide less reward for get-rich-quick efforts and shift business incentives toward long-run success over short-run profits. This is a concept President Trump endorsed just last week.

But if one wants to lower the taxes on return to saving, would adding indexing of capital gains to existing tax breaks be the best way to do it? Would it be superior, for instance, to a corporate income tax rate cut or a simple tax break for the investors living off their bonds?

Simply adding another capital gains tax cut would create new incentives to game the tax system. For example, if I can borrow at 5 percent and invest the money in an asset increasing in value by 5 percent per year, I have done no real saving and earned no real income. Yet, under current law, I can deduct the full 5 percent in interest costs in computing taxable income while paying tax at a reduced rate on my future realized capital gains. Exempting the effects of inflation only from capital gains that are subject to a preferential tax rate, but not adjusting interest deductions also, would increase the incentive to engage in these types of arbitrage games.

Taxing inflation is a problem that tax reformers might want to address. But offering revenue neutral options provides a litmus test for whether that is really the problem advocates for capital gains indexing want to address.

Beyond Wayfair, Can Nations and States Cooperate in Collecting Taxes?

Posted: July 9, 2018 Filed under: Uncategorized Comments Off on Beyond Wayfair, Can Nations and States Cooperate in Collecting Taxes?This column first appeared on TaxVox.

The brilliant Tax Notes columnist Marty Sullivan once summarized one of the great dilemmas in taxation: “It’s simply impossible to put a precise geographical subscript around ‘where’ taxes should be collected.” He mainly had in mind locating the source of capital income, but geography again reared its head recently when the Supreme Court’s South Dakota v. Wayfair, Inc. decision tackled the question of when states can require online retailers to collect sales taxes.

In both cases, it is difficult, if not impossible, for taxing jurisdictions to resolve these issues on their own. But they create important opportunities for these authorities to work together to develop solutions that are fair to taxpayers while assuring that government collects tax that is legitimately owed.

The issues are not easy to resolve. Countries struggle to sort out where a firm’s income is earned when its headquarters, production, marketing, research, and patents can be located anywhere in the world, when its sales routinely cross borders, and when some goods and services can be transferred or sold multiple times as intermediate products along the way toward a final sale.

This environment even affects charities, many of which routinely violate state and national laws simply by maintaining websites that can receive donations from anywhere but have not registered in every jurisdiction that might require it.

The Supreme Court’s Wayfair decision added to these boundary disputes. The Court ruled that states can obligate an on-line retailer to collect and remit sales taxes even if that firm’s website and physical facilities (such as manufacturing and headquarters sites) reside outside their jurisdiction.

Senator Heidi Heitkamp (D-ND) at a recent Tax Policy Center (TPC) event, as well as my colleague, Howard Gleckman, have noted how, for decades, Congress has failed to enact federal legislation to smooth out the administrative nightmares that online and catalog sales can create. But neither have the 50 states been able to agree on a coherent collections model.

However, there are examples of progress both internationally and among the US states.

My TPC colleagues Richard Auxier and Kim Rueben have detailed the various state efforts to use a streamlined sales tax agreement to address common measurement and registration issues caused by the evolution of on-line sales taxes.

Internationally, the OECD and G20 Base Erosion and Profit Shifting (BEPS) project laid out fifteen actions that nations can employ to increase transparency and adopt common standards for treating issues such as interest income, transfer pricing, and controlled foreign corporations.

So far, most of these multilateral efforts have been voluntary. Governments could be more aggressive in developing common practices if legislation or treaties made them mandatory. That big step is often opposed by those who benefit from the status quo, either through existing legislative favoritism or their ability to evade/avoid the laws. Yet pressure to resolve these issues continues to grow.

For example, the federal government could pre-empt some state actions by adopting a nationwide retail tax that it shares with the states according to a fixed formula. For many years, the federal government granted a credit against federal estate tax of up to 100 percent for payments of a state estate tax that included certain features. That gave states a significant incentive to adopt a common estate tax base since failing to do so effectively meant turning revenue over to the federal government.

Similarly, the European Union aims for a standardized tax base for the value-added tax, though its member countries may still set their own rates and are allowed some flexibility in defining their tax base.

In the face of growing complexity, even businesses are embracing common standards, at least up to a point. For instance, brick-and mortar retail firms have complained about their competitive disadvantage when on-line sellers do not collect tax for selling the same goods and services. In a sense, these firms are arguing for a common tax base to apply to both physical and on-line or mail-order sales.

Many firms’ finance and accounting officers complain about having to comply with a wide range of rules for defining income or sales tax bases among multiple jurisdictions. A multinational firm, for instance, may have to file income, sales, and value-added tax reports in thousands of jurisdictions. Even without foreign sales, a US firm may file hundreds of tax returns in the 50 states and numerous cities and counties. To address these concerns, third-party providers and software firms have jumped into this market by selling products to ease the burden on taxpayers and governments alike.

The evolution of the modern economy is only increasing pressure on taxing jurisdictions to cooperate and for federal systems to adopt laws or treaties that encourage or even require such cooperation among sub-national governments. Such efforts extend to registration, filing requirements, reporting, transparency, and definition of tax bases, and, sometimes, minimum tax rates.

These efforts always will be incomplete and ongoing, given legitimate pressures for tax competition and jurisdictional independence. But South Dakota v Wayfair, Inc. is an important step along this meandering path toward sometimes-workable conformity.

Why Government Budget Estimates Are Often Wrong

Posted: June 6, 2018 Filed under: Uncategorized Comments Off on Why Government Budget Estimates Are Often WrongThis column first appeared on TaxVox.

Government budget and tax analysts who estimate future federal revenues and spending are among the most talented people I know. They probably are a lot more accurate at what they do than typical academics or business consultants. However, their estimates frequently understate the true long-term costs of tax cuts or spending.

When estimators miss on the low side, it is often because they are trying to project costs of those government programs and tax subsidies that are both permanent or “mandated,” absent new legislation, and essentially open-ended.

Unlike programs where the government appropriates a fixed amount of money each year, the costs of mandated programs don’t need to be appropriated to be spent. Meanwhile, open-ended programs leave important determinants of cost, such as demand or price or definitions about who or what qualifies for the program, to decisions made by beneficiaries or service providers. When the two elements are combined, Congress effectively cedes long-term control of the costs to private individuals acting in their own, not necessarily the public’s, interest.

Estimation is simpler for mandatory programs or permanent tax benefits that are not open-ended. For example, estimators know that the cost of the child tax credit will equal the amount of the credit times the number of eligible children. Similarly, Social Security retirement benefits might grow rapidly but can be estimated with fair accuracy because they are set by formulas based on lifetime earnings that provide only limited discretion to recipients.

That is not so for Medicare, where beneficiaries and providers have often been allowed to appropriate resources to themselves. Consumers demand more access to healthcare treatment even as providers—who mostly are compensated based on volume—happily increase the supply of those treatments. Because there is little effective market discipline, health care provided by government creates a perfect fiscal storm. For example, suppose a drug company markets a new drug under government patent protection; it then sets a price; consumers demand the drug to address the ailment it treats; and—often—Medicare pays.

A similar phenomenon occurs with the open-ended tax subsidy for capital income, which is taxed at lower rates than ordinary income. Since ordinary income is taxed at a top rate of 37 percent while long-term capital gains are taxed at a top rate of 23.8 percent, taxpayers have an enormous incentive to recharacterize their income to benefit from the lower rate. The classic recent example: Hedge funds that have converted a share of their managers’ labor compensation income into lower-taxed long term capital gains income (carried interest).

Over the years, Congress and the IRS have played a game of whack-a-shelter with respect to preferential tax rates for capital income. Smart lawyers find a new way to turn ordinary income into lower-taxed capital gains, government (through either legislation or regulation) shuts it down, and then taxpayers and their advisors find another approach. That process makes it impossible to estimate government revenues for the long-run since estimators are supposed to assume the permanence of what is an inherently unstable law.

Forecasting capital gains revenue is even more difficult because investors can choose when to realize gains and, thus, pay the tax. As a result, gains can be earned over decades but are not taxed (and this generate no revenue) unless “realized” through an asset sale.

In a classic article, Nobel prize winning economist Joseph Stiglitz explained how individuals could take advantage of these arbitrage opportunities to reduce the taxes they pay. Given their voluntary nature, a large share of gains is never taxed because they are held until death—when their assumed cost in the hands of the heir is “stepped-up” to the market price at the time the person making the bequest passes away.

The newest example of an open-ended tax shelter is the Tax Cuts and Jobs Act’s 20 percent individual income tax deduction for income from pass-through businesses such as partnerships and sole proprietorships. It blows a hole in the government fisc so large than a Mack truck could be driven through it—as long as the operator is a sole proprietor. Congress attempted to limit the benefit to some types of earners and some types of businesses, but tax lawyers are busily finding ways to convert excluded businesses into qualified ones, and wage earners into independent business owners.

The structure of these types of laws makes estimating difficult enough. But two other factors make forecasting even more challenging.

The first is that the compounding of cost growth may take place years in the future and congressional scorekeeping conventions generally limit projections to the first 10 years, the so-called “budget window.” Underestimating a growth rate by a couple percent per year, for instance, compounds to a very large number over time.

The second is that estimators may be reluctant to project very large costs in the absence of empirical evidence. For example, the 20 percent tax deduction for pass-through income is new, and there is little information upon which to predict the magnitude of gaming that will occur. The revenue estimator doubtlessly will assume some gaming, but may not be imaginative and daring enough to forecast without much data a large multiplier for what lawyers or providers, in absence of further whack-a-shelter legislation, will invent for their clients.

Much is wrong with a system that allows enactment of open-ended mandatory spending programs and tax preferences. Until we repair that system, it is worth remembering there is a built-in bias towards underestimating their long-term costs.