Lost Generations? Wealth Building Among the Young

Posted: March 15, 2013 Filed under: Children, Columns, Economic Growth and Productivity, Income and Wealth, Race, Ethnicity, and Gender 19 Comments »The young have been faring poorly in the job market for some time now, a condition only exacerbated by the Great Recession. Now comes disturbing news that they are also falling behind in their share of society’s wealth and their rate of wealth accumulation.

Signe Mary McKernan, Caroline Ratcliffe, Sisi Zhang, and I recently examined how different age groups have shared in the rising net wealth of the U.S. economy. Despite the recent recession, our economy in 2010 was about twice as rich both in terms of average incomes and net worth as it was 27 years earlier in 1983. But not everyone shared equally in that growth.

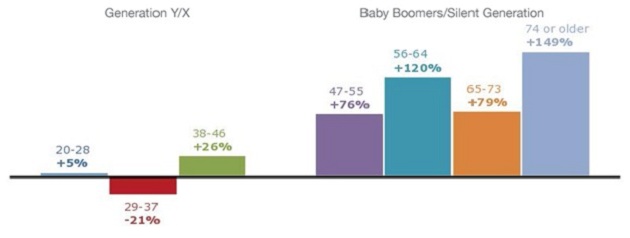

Younger generations have been particularly left behind. Roughly speaking, those under age 46 today, generally the Gen X and Gen Y cohorts, hadn’t accumulated any more wealth by the time they reached their 30s and 40s than their parents did over a quarter-century ago. By way of contrast, baby boomers and other older generations, or those over age 46, shared in the rising economy—they approximately doubled their net worth.

Older Generations Accumulate, Younger Generations Stagnate

Change in Average Net Worth by Age Group, 1983–2010

Source: Authors’ tabulations of the 1983, 1989, 1992, 1995, 1998, 2001, 2004, 2007, and 2010 Survey of Consumer Finances (SCF).

Notes: All dollar values are presented in 2010 dollars and data are weighted using SCF weights. The comparison is between people of the same age in 1983 and 2010.

Households usually add to their saving as they age, while income and wealth rise over time with economic growth. If these two patterns apply consistently and proportionately, then one might expect to see, say, a parent generation accumulate $100,000 by the time its members were in their 30s and $300,000 in their 60s, whereas their children might accumulate $200,000 by their 30s and $600,000 by their 60s.

This normal pattern no longer holds for the younger among us. However, this reversal didn’t just start with the Great Recession; it seems to have begun even before the turn of the century. The young increasingly have been left behind.

Potential causes are many. The Great Recession hit housing hard, but it particularly affected the young, who were more likely to have the largest balances on their loans and the least equity relative to their home values. If a house value fell 20 percent, a younger owner with 20 percent equity would lose 100 percent in housing net worth, whereas an older owner with the mortgage paid off would witness a drop of only 20 percent.

As for the stock market, it has provided very low returns over recent years, but those who hung on through the Great Recession had most of their net worth restored to pre-recession values. Bondholders usually came out ahead by the time the recession ended as interest rates fell and underlying bonds often increased in value. Also making out well were those with annuities from defined benefit pension plans and Social Security, whose values increase when interest rates fall (though the data noted above exclude those gains in asset values). Older generations hold a much higher percentage of their portfolios in assets that have recovered or appreciated since the Great Recession.

As I mentioned earlier, however, the tendency for lesser wealth accumulation among the younger generations has been occurring for some time, so the special hit they took in the Great Recession leaves out much of the story. Here we must search for other answers to the question of why the young have been falling behind. Likely candidates for their relatively worse status, many of which are correlated, include

- a lower rate of employment when in the workforce;

- delayed entry into the workforce and into periods of accumulating saving;

reduced relative pay, partly due to their first-time-ever lack of any higher educational achievement relative to past generations; - their delayed family formation, usually a harbinger and motivator of thrift and homebuilding;

- lower relative minimum wages; and

- higher shares of compensation taken out to pay for Social Security and health care, with less left over to save.

When it comes to conventional wisdom and media attention to distributional issues, there’s a tendency simply to attribute any particular disparity, such as the young falling behind in wealth holdings, to the growth in wealth inequality in society. But the two need not be correlated. Disparities can grow within both younger and older generations, without the young necessarily falling behind as a group.

Whatever the causes, we should also remember that public policy now places increased burdens on the young, whether in ever-higher interest payments on federal debts they will be left or the political exemption of older generations from paying for their underfunded retirement and health benefits. At the same time, state and local governments have given education lower priority in their budgets; pension plans for government workers now grant reduced and sometimes zero net benefits to new, younger hires; and homeownership subsidies post-recession increasingly favor the haves over the more risky have-nots.

Maybe, more than just maybe, it’s time to think about investing in the young.

It is right for society as a whole to invest in the young. All the young need to contribute is their time and hard work. We risk our money, they their time and hard work. We pay for education we think may help, they study what they think may help.

The error happened a generation ago when the contemporary conservative people decided that individuals reap the profit of their educations, and therefore they should pay for them. It’s not true. Elders are the guarantors, we train people and workers, and as the young take their place in the grown-up world, they get to make the decisions, and reap the benefits.

[…] Steurle, one of the co-authors of the study, points to a host of reasons for young people’s low net worth. Yes, they took a hit during the […]

[…] proposes a solution in his blog post about the report: “Start investing in the young” through education, pensions, and homeowner […]

Authors failed to mention the fact that the govt is guilty of currency debauchment, which is the only cause of the declining value of the dollar.

is the dollar declining?

check yo fax

Its about to get a lot worse for a lot of us that are age 55, any one who is working or married to a working government employee is going to have a day of pay cut each week. How is that going to help the economy or us? We are going to hurt worse. We are barely making the bills now.

It’s time to create widgets and time to find a marketplace. the boomers are ready to spend. Leave all traces of govt job behind. Get up. You can do it.

[…] Here are some depressing stats about my generation. […]

This “Wealth Building Among the Young” study by the Urban Institute misses the underlying causes of the flat line for youngest cohort. The youngest cohort has lower skills and low-skilled US jobs compete with lower cost workers in many other countries (globalization). While all US consumers benefit, the less-skilled workers in the US are hurt.

[…] proposes a solution in his blog post about the report: “Start investing in the young” through education, pensions, and homeowner […]

[…] proposes a solution in his blog post about the report: “Start investing in the young” through education, pensions, and homeowner […]

[…] Steurle, one of the co-authors of the study, points to a host of reasons for young people’s low net worth. Yes, they took a hit during the recession, […]

[…] Gene Steuerle: […]

[…] nuanced picture of household economics than just income, researchers Gene Steuerle and colleagues find that young adults under 40 have lost wealth in the past 10 years while those over 40 have […]

[…] X and Y have been left in the dust by the Baby Boomers. The Urban Institute recently released some research detailing the […]

[…] Steuerle, the study’s lead author, argues in an entry on his blog today that younger Americans have received less help than their elders in getting established […]

[…] Here’s a blog post by one of the authors on the study if you’d like to explore […]

Many of today’s young will receive housing and residual savings when their parents die. If they are in any kind of medical job, they will be employed caring for the aging population – although that can only go on for so long. As a late member of the Boomers, with a recently passed mother, what I received from her estate essentially kept me out of foreclosure. Getting a job would of course keep us out, although my government servicer is much more lenient then commercial banks. That is probably where the salvation of the young will come from, especially if they demand it – government programs including forgiveness of extreme student loan debt (which is a heavy burden for some unless inflation kicks off again).

Gгeat blog hегe! Additionally youг web site a lot սp fast!

What web host are you using? Can I am getting your associate link tօ үouг host?

I desire myy web site loaded ᥙр as quickly as yⲟurs lol.