Indexing Capital Gains For Inflation Addresses A Real Problem But Ignores Existing Law

Posted: August 23, 2018 Filed under: Uncategorized Comments Off on Indexing Capital Gains For Inflation Addresses A Real Problem But Ignores Existing LawThis column first appeared on TaxVox.

The idea of indexing capital gains for inflation is getting a lot of attention these days. Larry Kudlow, who heads the White House National Economic Council, has long suggested Treasury should do this by regulation, while several members of Congress have introduced bills to make the change by modifying the tax code. Exempting purely inflationary gains from tax can be a good idea in principle, but easily flawed in practice. To understand the consequences of such a shift, it is helpful to think about it in terms of a revenue-neutral tax change, not merely another budget-busting tax cut.

In a revenue-neutral context, indexing the basis of assets in computing capital gains could create significant winners and losers among investors. Ordinary shareholders could come out ahead, while private equity firms could be big losers. The effects would largely be dependent on rates of inflation and market returns.

First, though, some background: The argument for indexing rests on the principle that the income tax is meant to tax real, not nominal, income. If my investment returns 8 percent and inflation is 8 percent, then my real income gains are zero. Why should I pay tax on zero income?

To make matters worse, if we taxed all returns to saving with no offset for inflation, we could enormously overtax nominal returns to capital. If returns averaged 8 percent and but inflation was 4 percent, subjecting the full 8 percent nominal return to tax would essentially double the statutory tax rate on capital income.

In the 1984 Treasury study that led to the Tax Reform Act of 1986, these considerations led us to propose indexing the basis of assets that generate capital gains for inflation. But we attempted to apply the principle consistently. We would have indexed capital gains but also indexed other elements related to investment returns. We would have indexed depreciation allowances for inflation but also would have repealed the investment tax credit and set depreciation allowances to approximate economic depreciation. We also would have indexed interest receipts and interest payments for inflation.

Building on the old Treasury plan, imagine Congress indexes the taxation of capital income in a way that would neither gain nor lose revenues over time. Such a change would have many effects on the taxation of investment, but here are two significant ones:

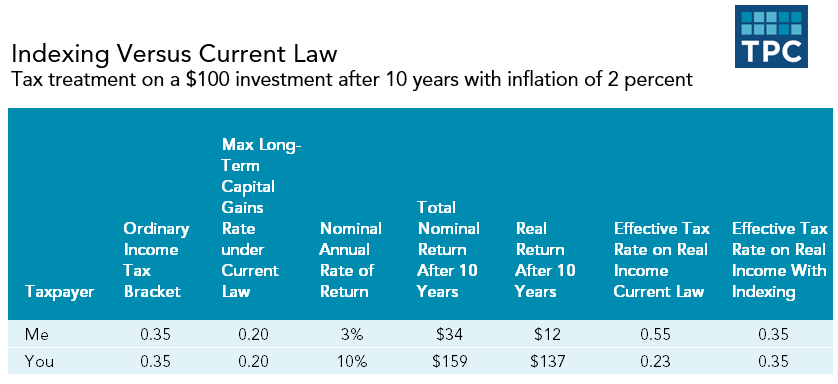

First, such a reform could redistribute the tax break to investors who tended to get lower returns over time from those who through luck or skill were big winners. Consider a reform proposal that substitutes indexing of capital assets for the preferential tax rate on long-term capital gains. The following table shows how this might work for a specific example.

For example, suppose you and I invested $100 ten years ago. Inflation was 2 percent annually over the period, and assume that we’re both in a 35 percent income tax bracket with a current maximum tax rate on long-term capital gains of 20 percent. Suppose that I earned a 3 percent nominal annual return per year and you made 10 percent. With indexing, we’d both reduce our gains by $22 (the amount of inflationary gain on the $100 investment). That would leave me with taxable income of about $12 out of my $34 profit. But you’d have taxable income of $137 out of your $159 gain (10 percent compounded over 10 years). With indexing and no preferential tax rate on capital gains income, we’d both pay the 35 percent rate but only on the real income amounts. Under current law, we’d each pay the 20 percent tax rate on our nominal capital gains ($6.80 tax for me and $31.80 tax for you). This translates in an effective tax rate on my real income of 55 percent and 23 percent for you. So, this proposal would treat all inflation adjusted returns the same, compared to current law, which favors investors with large inflation-adjusted gains.

Second, in a period of high inflation and moderate appreciation of assets, indexing gains for inflation while ending other preferential tax treatment for capital income might lower the amount of such income subject to tax. To illustrate this point, note that if inflation were 8 percent per year and the value of an asset increased at 8 percent per year, there would be no tax due under an inflation-indexing regime, but a positive tax liability under current law (even with the preferential tax rate on long-term gains). In contrast, in a period of low inflation and unusually high appreciation of asset values, such as in recent years, the indexing proposal likely would increase effective tax rates.

To see whether advocates really believe in the principle of excluding inflation from taxable gains, ask them if they would be willing to accept those consequences. In effect, would private equity and hedge fund managers be willing to transfer some of their existing tax breaks to help average investors?

I could make a solid case that such an exchange would be fairer and more efficient since it would provide less reward for get-rich-quick efforts and shift business incentives toward long-run success over short-run profits. This is a concept President Trump endorsed just last week.

But if one wants to lower the taxes on return to saving, would adding indexing of capital gains to existing tax breaks be the best way to do it? Would it be superior, for instance, to a corporate income tax rate cut or a simple tax break for the investors living off their bonds?

Simply adding another capital gains tax cut would create new incentives to game the tax system. For example, if I can borrow at 5 percent and invest the money in an asset increasing in value by 5 percent per year, I have done no real saving and earned no real income. Yet, under current law, I can deduct the full 5 percent in interest costs in computing taxable income while paying tax at a reduced rate on my future realized capital gains. Exempting the effects of inflation only from capital gains that are subject to a preferential tax rate, but not adjusting interest deductions also, would increase the incentive to engage in these types of arbitrage games.

Taxing inflation is a problem that tax reformers might want to address. But offering revenue neutral options provides a litmus test for whether that is really the problem advocates for capital gains indexing want to address.