Individuals Pay Very Little Individual Income Tax on Capital Income

Posted: September 13, 2018 Filed under: Uncategorized Comments Off on Individuals Pay Very Little Individual Income Tax on Capital IncomeThis column first appeared on TaxVox.

Most capital income earned never is taxed at the individual level, in part because assets are often not sold and their gains never subject to income tax, in part because capital income benefits from a long list of tax preferences, and in part because of outright evasion.

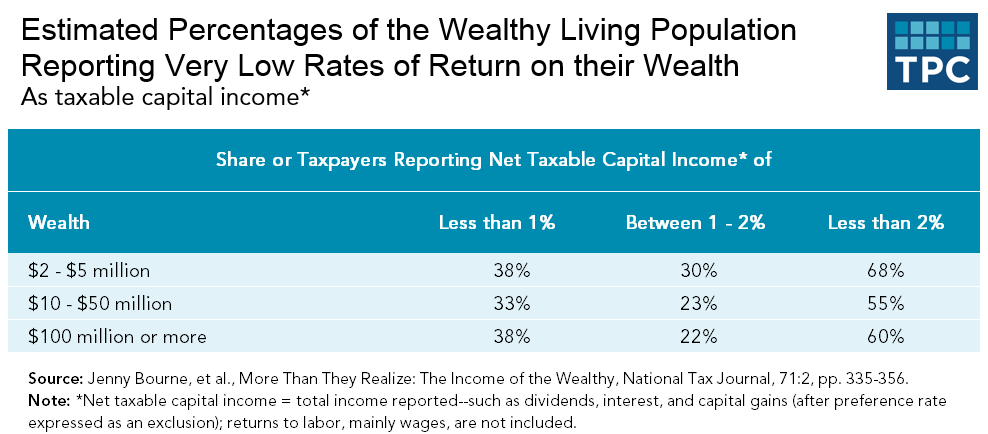

In a recently-published study, Jenny Bourne, Brian Raub, Joseph Newcomb, Ellen Steele, and I used estate tax data linked to individual income tax return data. In the study, we found that most wealthy individuals report an effective taxable return on their wealth of less than 2 percent on their individual income tax returns, with the richest filers reporting the lowest returns. That is, for each $1 million of wealth, the annual amount of taxable dividends, interest, capital gains, and other returns is less than $20,000. Among those with more than $100 million in net worth in 2007, close to 40 percent reported annual taxable returns of less than 1 percent of their wealth. More than two-thirds reported taxable returns of less than 2 percent.

These results are similar to what I found in a study covering the more inflationary 1970s. In yet another study, I found that a select group of owners of businesses and farms subject to estate tax reported even lower taxable returns. And in a book published in the early 1980s, I showed how net income from capital reported on all individual tax returns was less than one-third of total capital income in the economy.

These results are similar to what I found in a study covering the more inflationary 1970s. In yet another study, I found that a select group of owners of businesses and farms subject to estate tax reported even lower taxable returns. And in a book published in the early 1980s, I showed how net income from capital reported on all individual tax returns was less than one-third of total capital income in the economy.

Keep in mind, regardless of what they report on tax returns, top wealthholders often achieve very high actual returns on their assets. The merely wealthy commonly earn stock market returns of 7 to 10 percent per year, while truly rich investors often attained that status by earning even more. Warren Buffett revealed in one income tax return that he recognized only about 1/50th of 1 percent of his wealth as taxable income even though his primary asset, Berkshire-Hathaway stock, had been earning about 10 percent annually.

How do those with capital income achieve such low taxable earnings?

- Capital gains are not taxed until the assets are sold and the gains realized, providing an incentive to hold onto assets as they appreciate. As long as they are unsold, there is no taxable income to report.

- They take advantage of tax preferences. Real estate investors, for example, can defer taxable gains by swapping one piece of property for another through a “like-kind” exchange. The preferential tax rate on long-term capital gains acts as an effective reduction in taxable income, as it has been in most years when the preference was provided as an exclusion.

- Asset holders may avoid capital gains taxes by arbitraging tax laws. For example, they may offset gains with losses. Or they may establish tax shelters that produce current deductions in exchange for lightly taxed or untaxed capital gains.

- The returns from homeownership—the rent saving that comes from equity ownership—are not taxed.

- Retirement saving is heavily favored by the tax system, meaning that asset appreciation and capital income may not be taxed as they occur.

Homeownership and retirement saving provide the primary opportunities for middle-income and moderately-wealthy households to avoid or defer tax on capital income. As a result, they, too, pay limited tax on their returns from capital.

But for very wealthy individuals, the most common tax-avoidance strategy is simply to not sell assets at all and never realize the taxable gains. For example, a shareholder in a publicly traded company may accrue capital gains over time that remain untaxed until she sells her shares. If she holds the asset until death, those accrued but unrealized capital gains are excluded altogether from tax. The assets passed along as a bequest will have basis equal to the value at the date of former asset holder’s death.

Because so little capital income is taxed through the federal individual income tax, corporate and estate taxes have been important tools for taxing those with significant wealth. However, Congress has cut both those taxes over recent decades, most recently in the 2017 Tax Cuts and Jobs Act. Those reductions may have a far larger impact on the effective tax rate on capital income than changes in the statutory individual income tax rate since that levy only applies to income that is realized.

Unfortunately, the fight over capital income taxation usually focuses on how much is collected rather than on the most equitable or efficient way to tax it. Advocates on each side often will accept capital tax increases or decreases any way they can get them. Nor do the debates result in consistent treatment of people at different levels of wealth.

The Trump Administration reportedly is considering reducing taxes on capital income by indexing capital gains taxation for inflation. But at this point, the better question may be how best to distribute the taxes borne by capital owners, not simply how to tax some of them less.