Pushing on Air in a Balloon: Health Cost Growth and $1,000 Pills

Posted: November 11, 2014 Filed under: Columns, Health and Health Policy, Taxes and Budget Leave a comment »Numerous recent articles have tried to address whether health cost growth is slowing more permanently. Though I have entered that debate at times , I must admit that it’s a complex question for which there is no definite answer. Policymakers and private practitioners have improved some of the ways that health care is priced and delivered, and more improvements are no doubt forthcoming. But the stories of Gilead and its $1,000-a-pill Hepatitis C drug make one point entirely clear: improving health care costs selectively is like making indentations in a full balloon. Pushing down the air in one place merely makes it pop out somewhere else.

Consider how the government has designed health insurance, particularly Medicare. Essentially, it has delegated its constitutional powers of appropriation to private individuals and companies like Gilead. Congress doesn’t vote to spend more on hepatitis cures. It lets Gilead, along with patients and doctors, make that decision and then shift the costs back to other citizens. As long as Congress refuses to exercise its appropriations responsibility, every cost-saving measure could be nullified by a new Gilead.

The original sin of health insurance, public or private, has been to allow patients to demand and providers to supply more health care while pushing charges onto others. In the extreme, at a zero price to the patient per service received and a potentially unlimited supply of services for which more compensation and profits can be made, it is not surprising that health costs in this country have grown from about 5 percent of GDP in 1960 to around 17 percent today.

Many efforts aim to limit some of our bites of the forbidden apple but not others: fixed payments to accountable care organizations, health maintenance organizations, and preferred provider organizations; bundling of payments; limits on payments for re-admitted patients to hospitals; and so forth. Yet, yet… without absolution from the original sin.

Hospitals and doctors adjust in newer ways not restricted by selective limits. They add extra treatments and service providers. The ability to add on services is often voiced as the problem with fee-for-service medicine, where the quantity of services increases even for those whose prices are regulated or constrained. But there’s more to it than that; adding services is only one way that the air pops out somewhere else. In an industry with significant technological breakthroughs—and make no mistake, Gilead’s hepatitis drug is a major breakthrough—costs can be increased simply by charging a lot more for the new item or shifting services quickly toward areas of high profitability or compensation.

Even where a health improvement might be well worth the cost in one sense, it might still be unreasonable in another. In a typical open-market industry, we might be willing to pay a lot more for any particular good or service than we do, but competition among suppliers helps reduce costs. With the current design of health insurance, competition is fairly limited. My own brief examination of growth industries in the United States shows health is the one sector where above-average growth in the quantity of goods and services sold was accompanied by above-average growth in prices. Think of electronics, or telephones, or other advanced industries as examples of how increasing quantity usually pairs with decreasing prices.

The hepatitis C drug debate often confuses this value proposition in another way. Let’s accept that the $84,000 treatment with Sovaldi—or the newer, perhaps only $63,000 Hepatitis-C treatment with Harvoni (Gilead’s latest offering)—improves patient well-being and even life spans substantially. If the improvements make retirement years happier and longer, rather than being matched by greater productivity and more years of work, then Gilead and its beneficiaries still shift costs onto society, and health costs rise as a share of GDP.

Now, you might ask, what constrains the costs of inventions in non-health industries during those initial years when patents provide a potential monopoly? You and I do. If the cost is too high, many of us simply don’t buy the good or service. The company keeps prices lower to expand market share before competitors come along when the patent runs out. If the government says it will buy the new good or service for us, the limited-demand constraint that we otherwise provide is removed. Government simply cannot promise both that an inventor can charge what he wants for an invention and that the government will buy it for anyone who wants or needs it.

Thus, regardless of the rate at which health costs rise, it will remain unreasonable as long as the original sin of health insurance remains. Without true budget constraints, improvements will be limited because incentives are limited. With government programs, my own view is that every health care subsidy must be put into a budget, with limits raised over time by Congress but in a fair competition with other societal demands, be they education, defense, or currently unsubsidized forms of preventive health care.

Let Democrats use price controls. Let Republicans use vouchers. Let both work on other efficiency improvements that are more likely to be adopted when budgets are constrained. There is no one-time, permanent solution to how best to regulate this rapidly changing industry. With a constrained budget for each government program, however, Gilead would be unable to charge $1,000 a pill, or other health care providers would face a more rapidly declining price for their services, or both.

On the Progressivity of Obamacare

Posted: January 31, 2014 Filed under: Health and Health Policy, Shorts 3 Comments »Is the Affordable Care Act progressive in the most effective way?

In a very fine study, Henry Aaron and Gary Burtless at Brookings have looked at the ACA’s potential effects on income inequality and have preliminarily concluded that the ACA redistributes income—largely in the form of health benefits fits—to the poorest one-third of Americans. Most of the law’s additional subsidies—the expansion of Medicaid and subsidies for those buying insurance on the exchange—are highest for those with the lowest incomes. Offsets, such as some new taxes, tend to be concentrated less at those lower income levels.

What the Aaron and Burtless’ study was never intended to assess—and a lingering 21st century concern with almost all government health policies—is the ACA’s effectiveness and efficiency, both for the public in general and those with modest means in particular. For instance, many rewards of our government health policy have traditionally been captured by health industry providers, who are able to charge consumers higher prices. A program can be progressive, but still end up charging the public an additional $2 for $1.50 or $1 worth of care.

The ACA does at times attempt to deal with some of these issues and includes several experiments. But it was mainly directed at improving access, not reducing health costs. Reforms beyond the ACA still are required on that front regardless of which political party accedes to power.

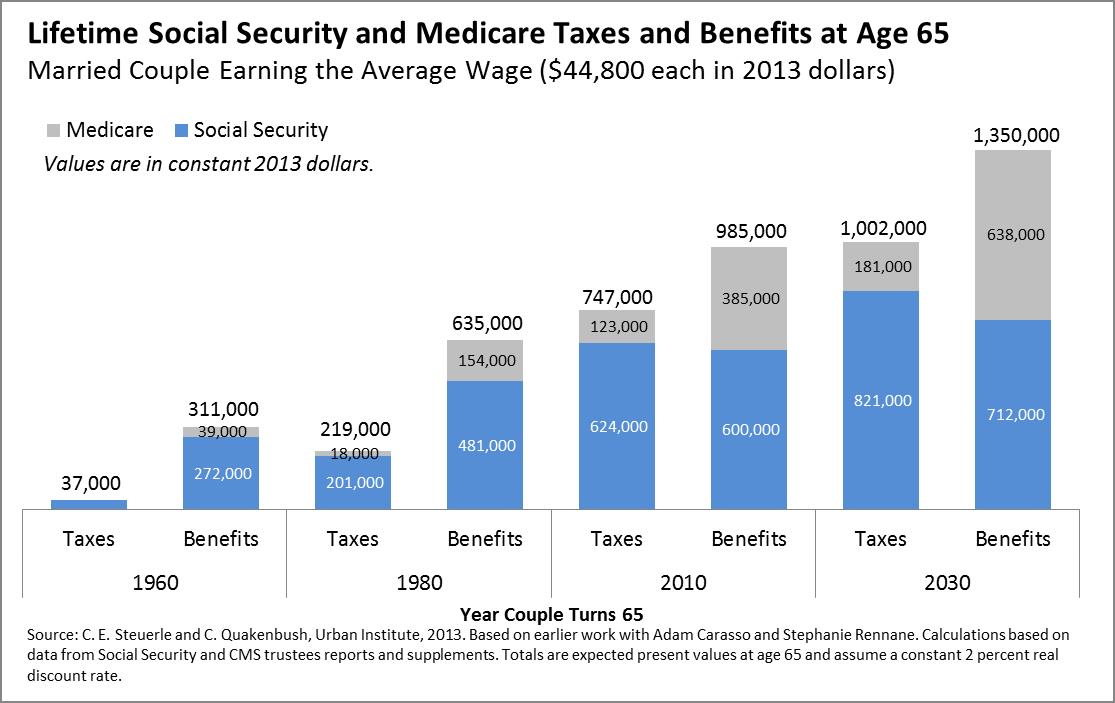

2013 Update on Lifetime Social Security and Medicare Benefits and Taxes

Posted: November 12, 2013 Filed under: Aging, Health and Health Policy, Income and Wealth, Shorts, Taxes and Budget 3 Comments »Our updated numbers for lifetime Social Security and Medicare benefits and taxes are now available, based on the latest projections from the Social Security and CMS actuaries for the 2013 trustees’ reports for OASDI and Medicare. Couples retiring today, with roughly the average earnings of workers in general, as well as average life expectancies, still receive about $1 million in lifetime benefits. This number is scheduled to increase significantly for future retirees and is higher for those with above-average incomes and longer life expectancies.

Little has changed on the Social Security side from our previous estimates, as the program has undergone no significant reform in recent years. Our estimates of present values of Medicare benefits for future retirees have decreased slightly from last year as slower health care cost growth has made its way into projections. By 2030, Medicare benefits (net of any premiums paid) are about 90 percent of last year’s estimates, still a significant multiple of Medicare taxes paid. (As in 2012, our numbers incorporate a Medicare cost scenario that assumes the “doc fix” and other adjustments will be extended, not the “current law” scenario in the trustees report.)

We have been publishing these numbers for a long time—and not without controversy over our intent. Our hope is simply that better and more complete information will help elected officials decide whether Social Security and Medicare are distributing taxes and benefits in the fairest and most efficient way possible, a decision we do not believe possible by looking only at annual numbers or how current, not future, retirees and taxpayers might fare. Therefore, we are delighted that in its most recent Long-Term Budget Outlook, the Congressional Budget Office for the first time also published estimates for lifetime Medicare benefits and taxes, as well as Medicare and Social Security combined. Using a slightly different methodology, CBO produces very complementary results. Differences derive from it using median-wage (rather than average-wage) workers, a 3 percent (rather than a 2 percent) real discount rate, and an assumption of Social Security claiming at 62 (rather than 65). As CBO also notes, expected benefits (and taxes, to a more limited extent) have grown over time for a number of reasons, including longer life expectancies, higher incomes, and rising health spending per person.

You Can Limit Our Deductibles, but it Won’t Reduce Our Health Care Bills

Posted: August 15, 2013 Filed under: Columns, Health and Health Policy, Taxes and Budget 2 Comments »When the Obama administration recently delayed its mandate on out-of-pocket health costs, experts and politicians started debating whether this delay affects our longer-term ability to implement Obamacare. I don’t think it does, but I also think we’re missing the bigger point. Once again, the United States is facing the total disconnect between our nation’s health care policies (whether Obamacare, Ryancare, or “your favored politician’s name here”-care) and the simple, unavoidable arithmetic of health care costs.

Let’s examine the latest example. Obamacare includes a mandate on insurers that out-of-pocket health care costs cannot exceed $6,350 for an individual or $12,700 for a family, numbers often cited as “catastrophic.” At first glance, these limits may sound high: six or twelve thousand dollars is a sizeable expense. But consider: households spend an average of $23,000 a year on health care. If it is considered catastrophic to ask some households to pay $12,000 in out-of-pocket expenses, then how can—or, more accurately, how do—all households cover costs that average almost twice as much?

A similar mathematical conundrum is playing out in another part of Obamacare. Congress determined that we shouldn’t have to pay more than 9 or 10 percent of our income for a moderately comprehensive health policy in the new health exchanges. But

consider: health costs now average about one-fifth of personal income and one-third

of money income. So how do we cover the difference?

The simple answer is that if we don’t pay in one way, we pay in another. Mandate any new limit on what consumers have to pay directly—on out-of-pocket deductibles, Medicare co-payment rates, drug costs under the Part D legislation pushed by President George W. Bush, or our share of the cost of health insurance in President Obama’s new health care exchanges—and those expenses don’t simply disappear. They just get tacked on somewhere else.

Of course, I’m only talking about averages. So you might object, “Well, at least I’m not the one who pays.” Perhaps true, but not as much as you might think.

Perhaps you are fairly healthy and have lower health needs. Insurance policies, however, shift costs from the unhealthy to the healthy. That’s as it should be, but the cost of insurance adds to any out-of-pocket cost. Moreover, since unhealthy households tend to have lower incomes to start with, and on average probably can’t cover even average costs of $23,000, healthy households probably pay at least that average amount and probably more to cover the income shortfalls from the less healthy. So being healthy doesn’t let us off the hook.

Perhaps you are middle class or even poor. The government’s health policies redistribute costs from those with higher incomes to those with lower incomes, including the retired. We might think that we avoid paying these high health costs by shifting tax burdens to the rich. Unfortunately, government health costs are already so high that the middle class has to share in the burden of paying for them.

More importantly, even if those health costs could be placed entirely on the rich, the rest of us would still pay what are called opportunity costs. When our elected officials require that a tax be spent on health care, they simultaneously decide that it can’t be spent on education or training or highways or other goods and services. The decline in education spending in recent years while health costs continued to rise provides only the latest piece of evidence.

Regardless of cost shifts to the healthy and those with higher incomes, we still pay a lot ourselves, only indirectly. In particular, we pay through lower cash wages when employers purchase health insurance, an important but often ignored aspect of the slow growth in cash compensation for over three decades. We also pay a decent amount through our own taxes, including federal income and Medicare taxes and all those state excise and sales taxes, often on businesses, that get passed onto us in the form of higher prices on what we buy. Finally, we pay a lot by borrowing from China, Japan, oil-exporting countries, and, more recently, the Federal Reserve, and then passing those outstanding balances and interest payments to our children.

And if paying a lot isn’t bad enough, these methods of paying help insure that we don’t always get our money’s worth. There’s fairly clear evidence that for every $100 of costs pushed into indirect and hidden budgets, our costs rise by more than $100 as health care providers find it easier to raise their prices.

So, the next time someone tells you that we can’t afford health costs that are only a fraction of what we actually pay, ask him where he thinks the extra money comes from.

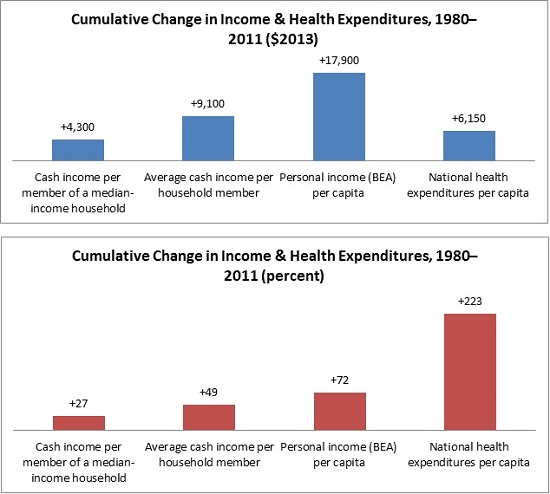

Growth in Income and Health Care Costs

Posted: June 4, 2013 Filed under: Columns, Economic Growth and Productivity, Health and Health Policy, Income and Wealth, Race, Ethnicity, and Gender 4 Comments »Worried about the stagnation of income among middle-income households? Or about the growth in health care costs? The two are not unrelated. In fact, middle-income families have witnessed far more growth than the change in their cash incomes suggest if we count the better health insurance most receive from employers or government. But is that all good news? Should ever-increasing shares of the income that Americans receive from government in retirement and other transfer payments go directly to hospitals and doctors as opposed to other needs of beneficiaries? Should workers receive ever-smaller shares of compensation in the form of cash?

The stagnation of cash incomes in the middle of the income distribution now goes back over three decades. Consider the period from 1980 to 2011. Cash income per member of a median income household, which includes items like wages and interest and cash payments from government like Social Security, only grew by about $4,300 or 27 percent over that period, when adjusted for inflation. From 2000 to 2010, it was even negative. Yet according to data from the Bureau of Economic Analysis, per capita personal income—our most comprehensive measure of individual income—grew 72 percent from 1980 to 2011.

How do we reconcile these statistics? By disentangling the many pieces that go into each measure.

Growing income inequality certainly plays a big part in this story: much of the growth in either cash or total personal income was garnered by those with very high incomes. So the growth in average income, no matter how measured, is substantially higher than the growth for a typical or median person who shared much less than proportionately in those gains. But personal income also includes many items that simply don’t show up in the cash income measures. Among them is the provision of noncash government benefits, such as various forms of food assistance.

Health care plays no small role. In fact, real national health care expenditures per person grew by 223 percent or $6,150 from 1980 to 2011, much more than the growth in median cash income. If we assume that the median-income household member got about the average amount of health care and insurance, then we can see how little their increased cash income tells them or us about their higher standard of living.

Getting a bit more technical, there’s a danger of over-counting and under-counting health care costs here. Some of the median or typical person’s additional cash income went to extra health care expenses, so the additional amount he/she had left for all other purposes was even less than $4,300. However, individuals pay only a small share of their health care expenses; the vast majority is covered by government, employer, or other third-party payments. So, roughly speaking, typical or median individuals still got well more than half of their income growth in the form of health benefits.

The implications stretch well beyond middle-class stagnation. Employers face rising pressures to drop insurance so they can provide higher cash wages. For instance, providing a decent health insurance package to a family can be equivalent roughly to a doubling of employer costs for a worker paid minimum wage. The government, in turn, faces a different squeeze: as it allocates ever-larger shares of its social welfare budget for health care, it grants smaller shares to education, wage subsidies, child tax credits, and most other efforts. Additionally, the more expensive the health care the government provides to those who don’t work, the greater the incentives for them to retire earlier or remain unemployed.

In the end, the health care juggernaut leaves us with good news (that our incomes indeed are growing moderately faster than most headlines would have us believe) as well as bad news (that health care remains unmerciful in what it increasingly takes out of our budget).

On Dementia, Cost-of-Living Adjustments, and the Right Way to Reform Programs for the Elderly

Posted: April 16, 2013 Filed under: Aging, Columns, Economic Growth and Productivity, Health and Health Policy, Income and Wealth, Taxes and Budget 4 Comments »While the increase in dementia among the elderly and the president’s proposal to change the index used to provide cost-of-living adjustments (or COLAs) to Social Security recipients have both received prominent headlines recently, the discussions have largely been independent of one another. Yet any principled attempt to reform our elderly programs, including Social Security, Medicare, and Medicaid long-term care, should consider them together.

A well-designed reform of elderly programs could and should accommodate some of the cost problems associated with dementia by back-loading a larger share of benefits in Social Security to older ages when these and other needs of old age increase. COLA adjustments, whatever their other merits, front-load the system by cutting back on benefits for the oldest the most and those in late middle age or their 60s hardly at all. That the president and Congress have limited ability to engage in these types of discussions and tackle multiple goals at the same time is yet one more example of how our political processes increasingly block us from fixing what ails us.

In a well-cited RAND study, Michael Hurd and his coauthors estimate that dementia-related care purchased in the marketplace will cost somewhere close to $0.25 trillion in 2040 (in 2010 dollars). That sounds like and is a lot of money, but Social Security and Medicare are expected to rise to cost over $3.5 trillion in that same year. Although I am greatly simplifying by ignoring such factors as how much of the $0.25 trillion would be covered by individuals and not the government or the effect of entitlement reform on costs, the raw comparison speaks for itself.

Simply put, some of the private and public budget problems associated with dementia, Alzheimer’s, and other growing problems for the older among the elderly could be addressed by providing higher cash benefits in older ages. Whatever the aggregate size of Social Security in general, one could pay for this reform by cutting back on benefits in younger ages of Social Security “old age insurance” receipt. This would not solve all the associated problems of dementia, but it would be a simple, effective, easy-to-administer step in the right direction. And, by concentrating benefits more in older ages, it would encourage working longer at a time when employment rates for the population as a whole are scheduled to decline.

But this is not the discussion we’re having. Instead, the president and many budget reformers put forward a proposal to adapt what many believe is a better measure of cost-of-living or price changes and apply it to almost all government programs, including Social Security. As a technical matter, a COLA adjustment doesn’t affect the growth in initial Social Security benefits for those who retire, only the inflation adjustment they get after they retire. At that point, they get a small annual cut—e.g. 3/10 of 1% the first year, 6/10 of 1% the second year, and so forth—that compounds every year in retirement, so that by the time beneficiaries are in their late 80s or 90s, some 25 or 30 years of lower COLAs add up to a cut in benefits of as much as 10 percent.

Social Security has never adjusted upward the earliest retirement age for increases in life expectancy. Instead, it reduced the earliest age from 65 to 62 in 1959 and 1962. As a consequence, the share of benefits going to those with 15 or more remaining years of expected receipt has risen dramatically over time, and the share to those with, say, less than 10 years of remaining life expectancy has declined. The COLA proposal, even with some very old age adjustments suggested by the president, would add to this long-term trend of making the program ever less available in relative terms for those in truly old age.

This is not to say that the COLA proposal should not be adopted. Who can oppose trying to measure something better? But attempts to fix systems like Social Security and other elderly programs one parameter or adjustment at a time cannot easily meet multiple worthwhile objectives. Similarly, efforts to back-load the system to meet the needs of true old age, as suggested here, should be coordinated with further adjustments—say, in minimum benefits—to avoid discriminating against those with shorter life expectancies.

With or without a better COLA, therefore, reform of Social Security and other elderly programs requires a more comprehensive approach if we are to meet the needs of old age as they evolve over time. Shouldn’t dementia be a higher priority than early retirement? If we’re going to spend $3 trillion or more annually on Social Security and Medicare by 2040, do we really think that the allocation of those funds be determined by formulas set in years like 1935 or 1965 or 1977, when much of the current system was cobbled together?

Who Is Insured or Not Insured by Government?

Posted: February 6, 2013 Filed under: Columns, Health and Health Policy, Taxes and Budget 3 Comments »One of the many dilemmas surrounding federal health care policies is that the government only partially insures most people when it subsidizes health care, but we want to pretend that once “insured” we are all entitled to the maximum health care available. This puts a lot of weight on the definition of “insurance” and creates misunderstandings about what the government does and does not do.

This issue came up in a column by Bruce Bartlett, who notes that Republicans may now oppose an individual mandate, but they do support (directly or indirectly) a mandate on hospitals to provide emergency care. Moreover, while ignoring their effective support of this mandate, and the effective taxes necessary to pay for it, Republicans maintain that the emergency-care mandate means that everyone has some amount of insurance coverage, however partial it may be.

This debate raises the question of what it means to be “insured.” No government plan covers everything. For those soon to have access to the exchange subsidy available through Obamacare, the “silver” and “bronze” plans that could be subsidized still cover only some costs. Medicaid, in turn, generally pays providers less than do other insurance plans; as one result, the more highly paid (and, often, more highly skilled) providers are less available. Similarly, Medicare does not cover all health services, including long-term care, and some doctors now refuse new Medicare patients, though that system’s payment rate is still higher than Medicaid’s.

You may argue that you want equal coverage—if some people get Cadillac coverage, everyone should. However, no elected official from either party seems willing to raise the taxes necessary to pay for such an expensive system. The reason is obvious: such health care would absorb all the revenue currently raised by the federal government and then some, leaving nothing for other government functions.

Even then, some people would step outside the system and buy a Mercedes policy, so inequality in health care would remain. Thus, the notion that everyone gets the same health insurance coverage, even in the most nationalized health system, is pure myth. But if people are not going to receive the Cadillac or Mercedes coverage from government that others obtain privately, how should Congress design policy with those multiple gaps in mind?

I don’t think there is any easy answer, but I do think that researchers and analysts should be more precise when reporting on “insurance” coverage. For example, the Congressional Budget Office produces counts of how many people would be insured under various options, but such estimates by themselves are misleading. Insured and not insured for what? For instance, if everyone received a simple (say, $5,000) voucher, with few restrictions other than that it must cover health care, almost everyone would buy at least a $5,000 insurance policy. On the other hand, if government dictated that the voucher had to be used to buy an expensive plan that many people couldn’t afford, then supplying a voucher would not produce fairly universal (yet partial) coverage.

Alternatively, one can’t assume that a highly regulated system will automatically provide whatever care is specified, since what it pays affects which providers participate in the system. The implicit assumption—and I am not judging it here—may be that many providers are so overpaid that cutbacks would have only limited effect on the care provided or the quality of the doctors and nurses who would accept a lower-paying career.

The ideal but difficult approach for researchers and budget offices, I think, is to note as best as possible what coverage is provided by regulation or subsidization of emergency rooms, Medicaid, Medicare, exchanges—indeed, of each government engagement in the health care economy. Note the expected gaps, whether in preventive care, higher-priced doctors, drugs, or other services. Finally, compare the extent to taxpayers and insured individuals avoid coverage gaps by paying higher taxes or more for their insurance.

In any case, a dichotomous count of who is “insured” or “not insured” is too simplistic. Almost any government health insurance policy is partial in care and cost. If Republicans want to claim that emergency room care is a type of insurance, then they should also acknowledge what is not insured through that mechanism and the implicit taxes on those who end up covering the emergency room cost. If Democrats want to claim that vouchers provide less insurance than a more regulated system, then they, too, should specify just what additional insurance they claim will be covered, at what cost to whom. Both parties should also make coverage comparisons for systems that are equally cost constrained.

What the Public Doesn’t Understand About Social Security and Medicare

Posted: January 30, 2013 Filed under: Aging, Health and Health Policy, Income and Wealth, Shorts, Taxes and Budget 6 Comments »An earlier short highlighted my research with Caleb Quakenbush into how much people pay in Social Security and Medicare taxes over a lifetime, and how much they receive in benefits. For instance, we found that a two-earner couple making an average wage who turned 65 in 2010 would have paid $722,000 in Social Security and Medicare taxes over their lifetimes, but would receive $966,000 in benefits.

These types of numbers often generate outraged debate over how much seniors are “owed” based on what they “paid in” to Social Security and Medicare.

But there is another, more philosophical, issue that these numbers cannot address. Americans do not pay their taxes into a personal account that they can take out, plus interest, when they retire. The money paid into Social Security and Medicare has always been chiefly paid out immediately to older generations. The only exception has been some trust funds which have always been modest in size and are shrinking. Thus, Social Security is effectively a transfer system from young to old, and always has been.

We may feel that because we transferred money to our parents, our kids, in turn, owe us. But we must take into account also how much they can or should afford for this task as opposed to their own current needs for themselves and their children. Think of a one-family society, where three kids support their parents, but then those three kids have no children of their own (or only one or two children). What those three kids gave their parents informs us only slightly on what they can or should get from their own children if there are none or fewer of them. Likewise, when demographics change and there are fewer workers to support an aging population, society has to make adjustments, regardless of what some may otherwise think is “fair” or what they think is their entitlement.

For articles inspired by this research, see a recent PolitiFact.